Analysis of the Collapse of Silicon Valley Bank

{kind=link}

My research, funded by the Research Experience and Apprenticeship Program (REAP) in the Hamel Center for Undergraduate Research, consisted of an analysis of the recent failure of Silicon Valley Bank (SVB) that occurred March 10, 2023. SVB was the sixteenth largest commercial bank in the United States and was headquartered in the region of Silicon Valley located in Santa Clara, California, catering mostly to technology-based customers. The banking sector generally follows a similar trend to the rest of the economy, in that if the economy is on a downturn, so is banking and vice versa. When SVB collapsed, consumers lost confidence in banking which increased fears of a recession.

I created a research plan which included gaining background knowledge on the bank from its founding to its collapse, writing a history section, conducting an empirical analysis, and communicating my findings in a full-length report. My research shows that the collapse of SVB has allowed the Federal Reserve to reevaluate policies and procedures to detect signs of danger more efficiently and include more regulation of regional banks. This research is significant in the finance and business world as a whole because it allows people to understand warning signs for big banks on the brink of failure and to how to avoid similar disasters in the future.

Background and History

To gather information about the bank, I centralized and cross-referenced news articles from places such as The Wall Street Journal and The New York Times that were published about the collapse and highlighted the bank’s history as well as the environment of the bank during the collapse. The news articles helped to craft the story of the bank’s beginnings to understand why Silicon Valley Bank failed and not other vulnerable firms such as similar midsized commercial banks like Citi Bank.

One of the bank’s major downfalls was its customer base, coming mostly from risky technology startups, and its large number of uninsured deposits which made the bank’s vulnerabilities more prominent. The collapse was years in the making with causes for concern starting in 2019 and worsening as time progressed. The state of the economy accelerated the bank’s failure as their main exposure came from rising interest rates that the Federal Reserve was pushing to combat record high inflation. Prior to the rise in interest rates, the bank had extra cash on hand and bought ten-year US Treasury bonds to grow their money securely. The rise in interest rates made it so the bonds were not worth as much as the bank originally paid for them, and the bank incurred a great deal of losses.

In my report, I showcased relevant events in SVB’s history such as the bank’s nationwide and global expansion, the burst of the dotcom bubble, as well as attempts at customer diversification. I also included some of the outside factors that accelerated the bank’s failure such as social media which increased consumer’s fear of the bank failure and preconceived notions about the bank including analysts’ forecasts. Before the collapse, the bank had a positive reputation in the startup tech industry and its failure shocked the banking sector with multiple other banks failing soon after SVB. Today, the banking sector is trying to navigate the impacts of the failures and adapting to new policy changes. Examining the foundation of the bank helped me understand what changed in the years prior to the collapse and how to avoid similar situations in the future.

Empirical Analysis and Event Study

After crafting the history portion of my report, the second part of my project was an empirical analysis that included an event study where I created various tables and graphs.

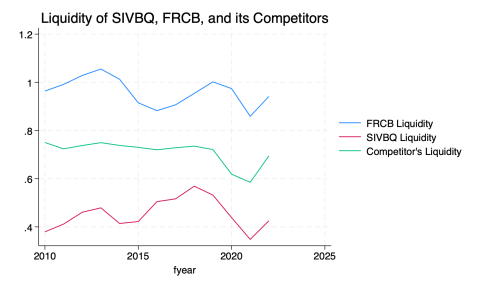

Figure 1: Using a ratio of SVB’s loans to deposits, which is a ratio for liquidity, the figure shows low liquidity at the time of failure and became one of SVB’s main exposures as their assets were not easily convertible to cash.

For the event study, I used CRSP and Eventus, two financial databases that helped to collect historic stock market returns for specified dates, and I was able to assess stock price reactions to major SVB event days for a sample of eleven competitor firms. I established event days by locating days with significant, negative SVB stock market returns as well as days where a negative announcement pertaining to SVB occurred; and the sample of competitors was determined by finding banks of similar size and type. As soon as the event days and competitor firms were finalized, the returns for SVB were compared to the mean returns of the competitors. Then, I determined if the events SVB experienced were based upon the bank’s wrongdoings or a result of the rest of the sector’s performance.

Figure 2: The ratio between cash and total assets shows how much a company’s assets consist of cash and short-term investments. SVB saw a significant peak in 2020 where they had excess cash and a sharp decline after that indicating that most of their assets did not consist of cash.

Coupled with the event study, I created a culmination of figures and tables to compare SVB and the competitors’ financial information over time to help craft a timeline of the collapse. To create the tables and graphs I used Stata software. Because Stata has a learning curve, especially for someone who has never used it before, it took some time to learn the functions so I could use it in its intended manner. After I became comfortable with the software, I was able to create tables and graphs that showcased SVB and the competitors’ cash, total assets, long term debt, liabilities, deposits, loans, and liquidity to get a sense of the abnormality of SVB’s financial information leading up to the collapse.

Some tables and graphs just showed SVB’s financial information over time while others showed the competitors, Silicon Valley Bank, and First Republic Bank, which was a competitor that collapsed soon after SVB. The tables and graphs revealed SVB’s main exposures such as a low level of liquidity, meaning their assets were not easily convertible to cash, compared to its competitors (Figure 1) and a stark increase in the ratio of cash to total assets in 2020 (Figure 2). Through analysis it became clear when the bank started seeing trouble.

Conclusion

The bank’s history, the event study, and the tables and graphs helped me generate an explanation as to why Silicon Valley Bank failed. Despite the collapse being years in the making, remiss supervisory from the Federal Reserve and SVB’s leadership made it so the bank was very vulnerable during a volatile time for the economy. Increased supervisory from the Federal Reserve needs to be practiced in the future which would include more frequent regulatory check ins for rapidly growing banks and their leadership as well as policies that provide support to banks in danger of collapse. The recent failure of multiple midsized banks has put the effects of high inflation and high interest rates into perspective leading to heightened concerns for a recession among consumers. Through improved policy, events similar to the collapse of SVB can be mitigated or prevented for the future.

With the conclusion of my research, I gained insight into myself as both a student and a researcher which includes how I time manage, communicate, and take initiative. I have expanded upon those skills, and they will translate into the rest of my education and into my career post-graduation. This project has opened my eyes to many research opportunities that I am avid to learn more about and to continue researching different topics in finance.

I would like to thank my mentors Stephen Ciccone and Steve Irlbeck for their guidance and support throughout my project. I would also like to thank the Hamel Center for Undergraduate Research for awarding me a Research Experience and Apprenticeship Program (REAP) grant as my experience has deeply impacted my education thus far. And lastly, I would like to thank Mr. Dana Hamel and Ms. Kathryn Early for funding my research.

Author and Mentor Bios

Melanie Yelle is a sophomore from Easton, Massachusetts majoring in business administration with concentrations in finance and information systems and business analytics. She is also minoring in dance. Melanie is a proud member of the Paul Scholars Program at the University of New Hampshire. As a student in Paul College, she did not have to start taking option classes right away, and she took advantage of the chance to explore her interest in finance by applying to the Research Experience and Apprenticeship Program (REAP). During the experience, Melanie learned that Silicon Valley Bank failed not only as a consequence of its own errors, but also due to a lack of oversight from the federal reserve. She chose to submit her research to Inquiry to publish her completed work and share her insights with students of other disciplines. Melanie hopes to become a financial analyst, but at the moment she knows there is a lot left for her to learn before embarking on her career. Pursuing her interest in finance through this research gave her new skills that will improve her internship and job application process.

Stephen Ciccone is an associate professor of finance in the Peter T. Paul College of Business and Economics at the University of New Hampshire. He holds bachelor's and master's degrees in accounting from the University of Florida and a Ph.D. in finance from Florida State University. He is a certified public accountant, formerly employed by Arthur Andersen. He has been a professor at the University of New Hampshire since 2000 and chaired the Accounting and Finance Department from 2013-2022. Among his research interests are stock return properties, analyst forecasts, and behavioral finance.

Steve Irlbeck is an assistant professor of finance in the Peter T. Paul College of Business and Economics at the University of New Hampshire. His current research interests are in empirical corporate finance. Dr. Irlbeck obtained a Ph.D. in finance in 2020 from the University of Iowa. He has experience teaching both undergraduate and graduate students in corporate finance, investments, risk management and insurance, and microeconomics.

Copyright © Melanie Yelle